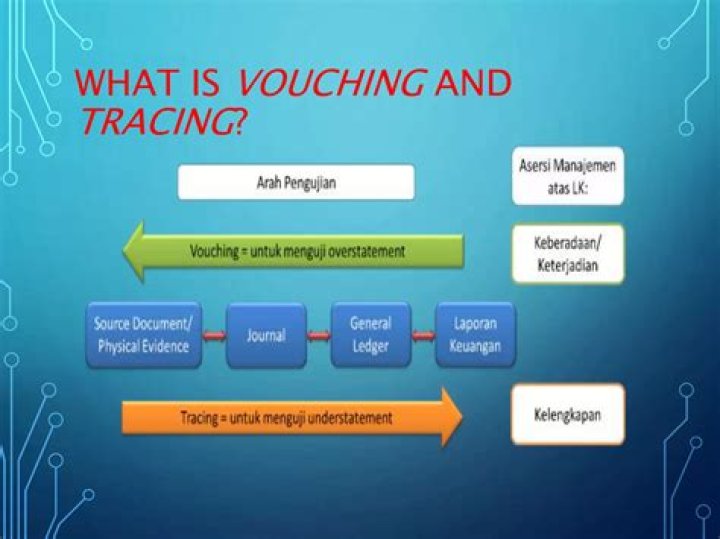

Tracing looks at a financial document and traces the path of that document all the way to the financial statements. Vouching goes the opposite direction. Vouching starts with a number on the financial statement and then you find the original document that supports that number. … Vouching provides evidence for occurrence.

What is vouching and tracing in audit?

When you vouch, you start with the financial statements and trace the transaction details to the source document. Vouching is typically used to address the existence assertion while tracing is used to address the completion assertion.

What is vouching in accounting?

Vouching is defined as the “verification of entries in the books of account by examination of documentary evidence or vouchers, such as invoices, debit and credit notes, statements, receipts, etc.

What is tracing in accounting?

Tracing is the process of following a transaction in the accounting records back to the source document. … Tracing is used to track down transactional errors, and also by auditors to verify that transactions were recorded properly.What is the purpose of vouching?

Objective of Vouching To check whether all the business transactions are properly recorded in the books of accounts or not. To see whether recorded transactions are duly supported by documentary evidence or not. To verify that all the documentary evidence is authenticated and related to business transactions only.

How does an auditor perform trace?

Tracing is done by looking at the unique document numbers and then moving to account books to locate the source document. Tracing is useful in tracking down transactional errors. The approach of audit tracing is used by the auditors to ensure and verify if transactions were recorded properly.

What are the 5 financial statement assertions?

The different financial statement assertions attested to by a company’s statement preparer include assertions of existence, completeness, rights and obligations, accuracy and valuation, and presentation and disclosure.

What is footing in auditing?

What Are Footings? In accounting, a footing is the final balance when adding all the debits and credits. Debits are tallied, followed by credits, and the two are netted to compute the account balance. Footings are commonly used in accounting to determine final balances to be put on financial statements.Is tracing a test of controls?

Auditors use tracing to check the internal controls of the client for effectiveness, get an idea of the processes behind transactions and balances, and to verify the completeness assertion of transactions.

Is vouching a substantive test?Because the purpose of the vouching technique is to obtain evidence about a recorded item in the accounting records, the direction of the search for the supporting documents is crucial. … Re-performance – The re-performance of client activities involved in the accounting process is a common substantive technique.

Article first time published onWhat are the types of voucher?

- Debit or Payment voucher.

- Credit or Receipt voucher.

- Supporting voucher.

- Non-Cash or Transfer voucher (Journal voucher)

What is teeming and lading?

A term used to describe attempts to hide the loss of cash received from one customer by using cash from other customers to replace it. This fraud can carry on by using cash from other customers in the same way. An investigation into teeming and lading has been raised against the organisation.

How do you examine vouchers?

Serial Number: He should see whether all vouchers are consecutively numbered and filed in order of the entries in the various books. 4. Date, Name, Amount, etc.: The auditor should check date, name of the party to whom the voucher is issued, the name of the party issuing the voucher, and the amounts, etc.

What is difference between accounting and auditing?

Accounting maintains the monetary records of a company. Auditing evaluates the financial records and statements produced by accounting.

WHO removes internal auditor?

Explanation: Internal auditor can be removed by the company management; whereas external auditor can be removed by the shareholders of the company.

What is the procedure of vouching?

Definition: Vouching is a procedure followed in the process of the audit to authorise the credibility of the entries entered in the books of accounts. In simple and easier words, it is a precise investigation of the presented documents of the firm by an auditor to check the correctness and accuracy of such documents.

What are the 7 audit assertions?

- Accuracy. The assertion is that all information disclosed is in the correct amounts, and which reflect their proper values.

- Completeness. The assertion is that all transactions that should be disclosed have been disclosed.

- Occurrence. …

- Rights and obligations. …

- Understandability.

What are the 7 assertions?

- Existence. The existence assertion verifies that assets, liabilities, and equity balances exist as stated in the financial statement. …

- Occurrence. …

- Accuracy. …

- Completeness. …

- Valuation. …

- Rights and obligations. …

- Classification. …

- Cut-off.

What is neutrality in accounting?

Neutrality requires that management prepare completely unbiased financial statements. For example, a company with information about a probable lawsuit must report it on their financial statement notes. Withholding this information would make the financial statements unreliable to outside investors and creditors.

How do you audit vouching?

- Check whether the vouchers are printed, numbered and arranged in the order of the date of occurrence of transactions.

- The entries in the books of accounts should also be numbered and the number and date should correlate with the concerned voucher.

What assertions does vouching test?

While tracing tests the completeness assertion, auditors usually perform vouching to test the occurrence or existence assertion in the audit. Hence, these two procedures provide two different types of evidence (completeness vs. occurrence or existence).

What are the purposes of audit documentation?

Purposes of Audit Documentation1It provides evidence of auditors’ basis for a conclusion about the achievement of the overall objective.2It provides evidence showing that audit work was properly planned and performed in accordance with ISAs and other legal and regulatory requirements.

What are the 5 internal controls?

There are five interrelated components of an internal control framework: control environment, risk assessment, control activities, information and communication, and monitoring.

What is the meaning of detection risk?

Detection risk is defined as ‘the risk that the procedures performed by the auditor to reduce audit risk to an acceptably low level will not detect a misstatement that exists and that could be material, either individually or when aggregated with other misstatements. ‘

What is assertion level?

So the “assertion level” is the level at which statements are presented as completely true. E.G. Management tells the auditor the financial statements show a true valuation of inventory – management are formally “asserting” this statement as being correct, so we call this at the “assertion level”.

What is tick and tie?

You may be wondering what “tick and tie” means. It refers the action an accountant performs when he agrees one financial statement number to another. … This is the purpose of ticking and tieing numbers: to ensure that the financial statements are correct.

What is double rule?

The doubling rule states that if a one syllable word ends with a vowel and a consonant, double the consonant before adding the ending (e.g. -ed, -ing).

What is footed and cross footed?

To “foot” a column of numbers means to total the rows and compare to a grand total. To “cross foot” a row means to total across the numbers in each column.

What is Reliance strategy?

A reliance strategy means that the auditor intends to rely on Internal Audit, or others, rather than performing more “hands on” audit procedures in order to obtain audit evidence for themselves.

Can you eliminate sampling risk explain?

Can you eliminate sampling risk? Explain. Yes, sampling risk can be eliminated by testing the 100% of the population. It is because if the sample size were increased to include all the items in a population, there would be no sampling and therefore no sampling risk.

Why do we test controls?

The aim of tests of control in auditing is to determine whether these internal controls are sufficient to detect or prevent risks of material misstatements. … However, if they are found to be weak or ineffective, the control risk is high. This means that the auditor will have to perform additional tests during the audit.