A familiarity threat exists if the auditor is too personally close to or familiar with employees, officers, or directors of the client company.

What is familiarity risk?

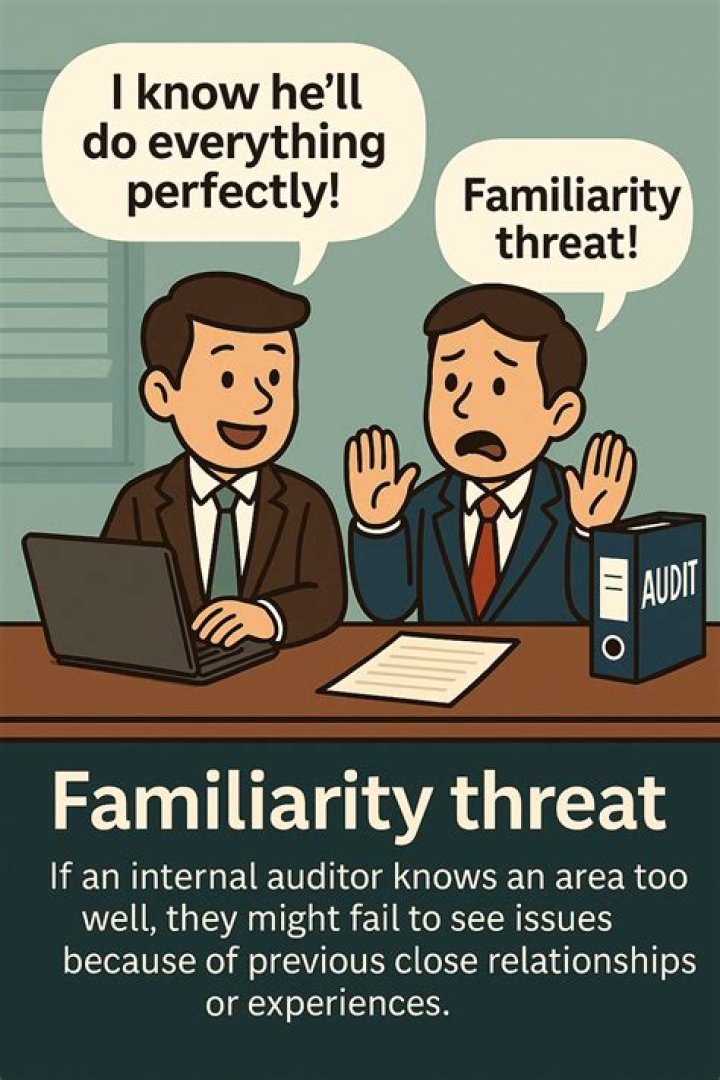

The familiarity threat is when an auditor allows their familiarity with the client to threaten their independence. Usually, their familiarity leads them to become too trusting of the client and can cause them to make biased decisions.

How do you solve familiarity threats?

- Changing the role of the senior personnel on the attest engagement team or the nature and extent of the tasks the senior personnel perform.

- Having a professional accountant who was not included on the attest engagement team review the work of the senior personnel.

What is familiarity in auditing?

The relationship between the directors and the auditors has been termed the `Familiarity’ or `Trust Threat’ (Chartered Accountants Joint Ethics Committee, 1995). This is argued to exist where the auditor is over influenced by the personality and qualities of directors or where the auditor knows the client too well.Which of the following is not an example of a familiarity threat?

d. Occurs when a firm, or a member of the assurance team, promotes, or may be perceived to promote, an assurance client’s position or opinion to the point that objectivity may, or may be perceived to be, compromised. 59.

What does professional skepticism mean?

Professional skepticism is an attitude that includes a questioning mind and a critical assessment of audit evidence. … In exercising professional skepticism, the auditor should not be satisfied with less than persuasive evidence because of a belief that management is honest.

What is a self interest threat?

Section 200.8 A6 describes self-interest threat as: “The threat that a member could benefit, financially or otherwise, from an interest in, or relationship with, the employing organisation or persons associated with the employing organisation. … This would help to safeguard against the threat.

What are ethical threats?

An ethical threat is a situation where a person or corporation is tempted not to follow their code of ethics. An ethical safeguard provides guidance or a course of action which attempts to remove the ethical threat.What are the factors that militate against auditors independence?

(1999) listed four factors militating against independence constraints to independence, and they include Instances where auditor depends on client for economic wellbeing, competing for Audit market; the regulatory guidelines and the provision of services unrelated to auditing duties (NAS).

What impairs auditor independence?Independence will be considered to be impaired if, during the period of a professional engagement, a member or his or her firm had any cooperative arrangement with the client that was material to the member’s firm or to the client.

Article first time published onHow do you avoid self review threats?

The most effective safeguard against the self-review threat is the segregation of teams. Audit firms that provide non-audit services to clients must use separate members for each assignment. This way, they will never face the threat of having to review their own work.

How do you ensure auditor independence?

The SEC rules on audit independence are often organized into five key areas: (A) Prohibited Non-Audit Services; (B) Audit Committee Pre-Approval of Services; (C) Partner Rotation; (D) Conflict of Interest; and (E) Increased Communication and Disclosure.

What is audit risk?

Audit risk is the risk that financial statements are materially incorrect, even though the audit opinion states that the financial reports are free of any material misstatements. Audit risk may carry legal liability for a certified public accountancy (CPA) firm performing audit work.

What is safeguard in audit?

Safeguards are actions or other measures that may are appropriate to eliminate threats or. reduce them to an acceptable level. • Safeguards are actions or other measures that may will reasonably eliminate threats or reduce. them to an acceptable level.

What are threats to fundamental ethical principles?

Threats to compliance with the fundamental principles Compliance with the fundamental principles may potentially be threatened by a broad range of circumstances. Many threats fall into the following categories: self-interest • self-review • advocacy • familiarity • intimidation.

Who is the person that has the authority to suspend or remove a member of the Professional Regulatory Board of Accountancy on valid grounds and after due process?

The Professional Regulation Commission has the authority to remove any member of the Board of Accountancy for negligence, incompetence, or any other just cause. b.No person shall be appointed as a member of the Board of Accountancy unless he has been in the practice of accountancy for at least 10 years, among others.

What is intimidation threat?

Intimidation Threat An intimidation threat exists if the auditor is intimidated by management or its directors to the point that they are deterred from acting objectively. Example. ABC Company is unhappy with the conclusion of the audit report and threatens to switch auditors next year.

What are the five codes of ethics?

- Integrity.

- Objectivity.

- Professional competence.

- Confidentiality.

- Professional behavior.

Which of the following is an example of self interest threat?

Self interest threat Examples include: When the auditor or a member of their family owns shares in a client. They would directly benefit from increases in client profits and would be reluctant to raise any concerns that could adversely affect the performance of the client.

What are threats to professional skepticism?

Some of the potential threats to professional skepticism that may exist at the Individual Auditor level include: Judgment traps and biases, lack of knowledge and expertise. Deadline pressure, inherited preferences, and expectations.

What are two common judgment traps?

Prawitt identified confirmation bias and a phenomenon the white paper calls judgment “triggers” as two particularly damaging “traps” that lead to poor judgment and decisions.

What is Operation Broken gate?

Internally designated “Operation Broken Gate,” the Enforcement Division’s efforts seek to identify auditors who fail to carry out their duties and responsibilities consistent with professional standards.

Can an auditor ever be truly independent?

Ultimately, as long as audit appointments and fees are determined by the company being audited, the auditor can never truly be economically independent of the client. That is why there are broader codes of conduct which govern the relationship between both parties.

Why might an auditor issue a disclaimer of opinion after an audit?

When an auditor issues a disclaimer of opinion report, it means that they are distancing themselves from providing any opinion at all related to the financial statements. … They may not have been able to decipher the correct nature of some transactions or to secure enough evidence to support good financial reporting.

How many years can an auditor audit the same company?

Public companies are supposed to rotate auditing firms after 10 years, though they can extend the period to 20 years if they put out bids for audit services from other firms within the 10 years.

Can an auditor go to work for a client?

The SEC has no prohibition against an auditor leaving his job to work for a client, but it does require the auditor to sever any financial ties to the auditing firm. That the SEC and accounting industry’s professional standards permit an auditor to take a job for a client is telling, according to Andersen.

Can I audit my brother's firm?

As per section 141(3)(d)(i), a person shall not be eligible for appointment as an auditor of a company, who, or his relative or partner is holding any security of or interest in the company or its subsidiary, or of its holding or associate company or a subsidiary of such holding company.

What is undue influence threat?

The undue influence threat is the threat that a member will subordinate his or her judgment to an individual associated with a client or any relevant third party due to that individual’s reputation or expertise, aggressive or dominant personality, or attempts to coerce or exercise excessive influence over the member.

Can your accountant also be your auditor?

Your accountant can act as the company’s auditors if they: don’t fall into one of the disallowed categories (see ‘Who can my company appoint as an auditor?’ above); don’t take part in the management of the company at all; and.

What auditors Cannot do?

First and foremost, auditors do not take responsibility for the financial statements on which they form an opinion. The responsibility for financial statement presentation lies squarely in the hands of the company being audited. … But, in short, the auditor may not assume the role and duties of management.

Can auditors audit their own work?

They are conducted in an impartial and objective manner following an agreed scope and procedures. Audits are used to gather facts and determine the degree to which requirements are being met. … Remember, an auditor must be impartial and objective, and cannot audit their own work.