There is no rule that says you have to refinance with your current lender. In fact, many homeowners refinance with a different mortgage company. Sometimes it’s smart to go with your current lender; at other times you’ll do better with a new one.

Does it make sense to refinance with the same bank?

There is no rule that says you have to refinance with your current lender. In fact, many homeowners refinance with a different mortgage company. Sometimes it’s smart to go with your current lender; at other times you’ll do better with a new one.

How much does a mortgage company make on a refinance?

Lenders generally pay a higher commission than borrowers do. When lenders compensate mortgage brokers, they typically pay between 0.5% and 2.75% of the total amount of the loan.

Can you refinance with a different mortgage company?

You don’t have to refinance with your current lender. If you choose a different lender, that new lender pays off your current loan, ending your relationship with your old lender. Don’t be afraid to shop around and compare each lender’s current rates, availability and client satisfaction scores.What is the average closing cost on a refinance?

Mortgage refinance closing costs typically range from 2% to 6% of your loan amount, depending on your loan size. National average closing costs for a refinance are $5,749 including taxes and $3,339 without taxes, according to 2019 data from ClosingCorp, a real estate data and technology firm.

Can I refinance a mortgage that was not reaffirmed?

First of all, there is no legal reason at all why you can’t refinance a loan that was not reaffirmed. … Without an agreement the loan is discharged but the lien remains against the property. As long as you make the payments and stay current you get to keep the home.

Why do lenders want you to refinance?

Your servicer wants to refinance your mortgage for two reasons: 1) to make money; and 2) to avoid you leaving their servicing portfolio for another lender. Some servicers will offer lower interest rates to entice their existing customers to refinance with them, just as you might expect.

Can I switch lenders when refinancing?

Know that you’re free to switch lenders at any time during the process; you’re not committed to a lender until you’ve actually signed the closing papers. But if you do decide to switch, re–starting paperwork and underwriting could cause delays in your home purchase or refinance process.Does refinancing hurt credit?

Taking on new debt typically causes your credit score to dip, but because refinancing replaces an existing loan with another of roughly the same amount, its impact on your credit score is minimal.

Is it a good idea to switch mortgage?You could make significant savings on your mortgage if you can switch to a lower interest rate. … Notify you, if you are on a variable rate (but not a tracker), if you can move to a cheaper rate due to a change in your loan-to-value ratio. You will need to provide an up-to-date valuation for this.

Article first time published onWhat are the risks of refinancing your home?

Many consumers who refinance to consolidate debt end up growing new credit card balances that may be hard to repay. Homeowners who refinance can wind up paying more over time because of fees and closing costs, a longer loan term, or a higher interest rate that is tied to a “no-cost” mortgage.

How do you know if refinancing is worth it?

Mortgage rates have gone down So how much should mortgage rates fall before you consider whether refinancing is worth it? The traditional rule of thumb says to refinance if your rate is 1% to 2% below your current rate. Make sure to factor in your current loan term when considering refinance though.

Why do banks push refinancing?

Your financial institution wants to keep you happy Another reason lenders might encourage you to refinance is to prevent you from seeking out a lower rate elsewhere. By offering the best rates, banks are able to keep their account holders’ business, and ensure a positive experience to promote future business.

Why are closing costs so high on a refinance?

Why does refinancing cost so much? Closing costs typically range from 2 to 5 percent of the loan amount and include lender fees and third–party fees. Refinancing involves taking out a new loan to replace your old one, so you’ll repay many mortgage–related fees.

How can I avoid paying closing costs?

- Look for a loyalty program. Some banks offer help with their closing costs for buyers if they use the bank to finance their purchase. …

- Close at the end the month. …

- Get the seller to pay. …

- Wrap the closing costs into the loan. …

- Join the army. …

- Join a union. …

- Apply for an FHA loan.

What happens to my escrow when I refinance?

When you refinance a loan, the original escrow account remains with the old loan. … All the property tax and insurance payments you have made to that account, since the last payment was made, will be returned to you, usually within 45 days via wire transfer or check.

What's the catch with refinancing?

The catch with refinancing comes in the form of “closing costs.” Closing costs are fees collected by mortgage lenders when you take out a loan, and they can be quite significant. Closing costs can run between 3–6 percent of the principal of your loan.

What percentage difference Should you refinance?

The traditional rule of thumb is that it makes financial sense to refinance if the new rate is 2 percent or more below your existing interest rate. The new rate on a refinance must provide enough savings in monthly mortgage payment to justify the cost of refinancing.

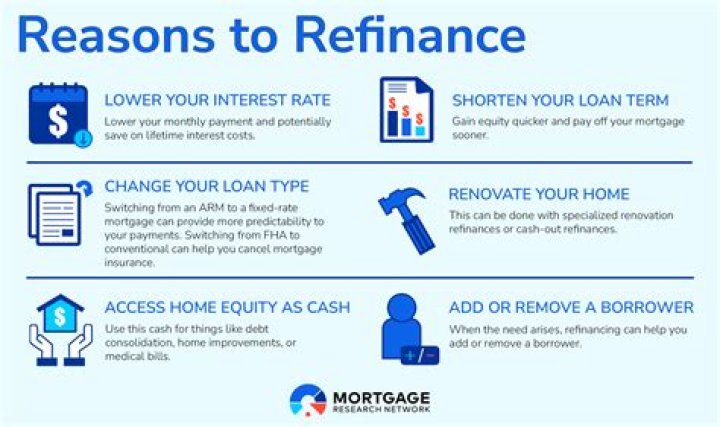

Does refinancing lower interest rate?

Refinancing can lower your monthly mortgage payment by reducing your interest rate or increasing your loan term. Refinancing also can lower your long-run interest costs through a lower mortgage rate, shorter loan term or both.

What happens if you don't reaffirm mortgage?

If you do not reaffirm the mortgage, your personal liability for paying the debt represented by the promissory note is discharged in your bankruptcy case. … The company can foreclose the mortgage and force a foreclosure sale if you stop making payments.

How do I get my mortgage reaffirmed?

Reaffirming a mortgage debt requires a comprehensive multi-page reaffirmation agreement that must be filed with the court. The reaffirmation agreement also requires the debtor’s bankruptcy attorney to indicate that he or she has read the agreement and that it does not impose any undue hardship on the client.

What does it mean to not reaffirm mortgage?

A reaffirmation agreement is an agreement made between a creditor and the debtor that waives discharge of a debt that would otherwise be discharged in bankruptcy. … When a debtor does not reaffirm a mortgage loan, the lender will stop reporting the loan on the debtor’s credit report.

What is a good credit score?

Although ranges vary depending on the credit scoring model, generally credit scores from 580 to 669 are considered fair; 670 to 739 are considered good; 740 to 799 are considered very good; and 800 and up are considered excellent.

Is it bad to refinance your house multiple times?

There’s no legal limit on the number of times you can refinance your home loan. However, mortgage lenders do have a few mortgage refinance requirements that need to be met each time you apply, and there are some special considerations to note if you want a cash-out refinance.

Does refinancing affect taxes?

Mortgage interest and itemizing deductions Something to keep in mind is that refinancing your mortgage can significantly reduce your total tax deductions. Refinancing to a lower mortgage rate means you’ll be paying less interest, which means you’ll have less mortgage interest to deduct when tax time comes around.

Can I walk away from a rate lock?

You can back out of a mortgage rate lock, but there are consequences. Backing out of a rate lock means giving up the application you’ve put time and money into. You’ll have to start your mortgage application over from the start, and you’ll likely have to re–pay fees like the credit check and home appraisal.

Does locking a rate commit you to a lender?

A rate lock commits the lender to honoring the rate at closing as long as it occurs before the lock expires. To a degree, it also commits the buyer to using that lender to close the loan.

How do I change my mortgage from one company to another?

The only way to change mortgage servicers is to refinance your loan and move to a lender that services the loans they originate. Keep in mind, just because a company services a loan today doesn’t mean they’ll continue to do so long term. The industry is always changing.

What happens when you switch your mortgage?

You can change your interest rate, payment frequency and prepayment options, but your mortgage amount and amortization period must remain the same. … Then your new lender will pay out your mortgage with your old lender, and issue you a new mortgage with them.

Can you change mortgage before fixed term ends?

Yes, you can. You might have to pay Early Repayment Charges (ERCs) and exit fees to do it, but there’s little stopping you from leaving a fixed-rate mortgage deal before the end of the agreed term. There’s nothing legally stopping you leaving a fixed term before it ends.

How soon can you remortgage before fixed rate ends?

Ideally, you should start planning to remortgage around six months before your fixed rate period ends. Acting early can also help you avoid extra payments.