Short-run price is determined by short-run equilibrium between demand and supply. Thus, the average variable cost sets a minimum limit to the price in the short run, since at prices below it no amount of output will be produced and offered for sale. …

What is market price How is it determined under perfect competition?

In a perfectly competitive market individual firms are price takers. The price is determined by the intersection of the market supply and demand curves. The demand curve for an individual firm is different from a market demand curve.

How are price and output determined under monopoly in the short run?

Short-run refers to that period in which a monopolist cannot change the fixed factors. However, the monopolist is free in determining price due to lack of competition. … Therefore, he/ she will adjust the output in such a way that the marginal cost and marginal revenue are equal.

How output is determined in the short run?

In the short run, output is determined by both the aggregate supply and aggregate demand within an economy. … The equilibrium is the point where supply and demand meet. According to Hume, in the short-run, and increase in the money supply will lead to an increase in production.How are price and output determined under it?

The market price and output is determined on the basis of consumer demand and market supply under perfect competition. In other words, the firms and industry should be in equilibrium at a price level in which quantity demand is equal to the quantity supplied.

How is short run price determined under monopolistic competition?

In monopolistic competition, profits are maximized at a point where marginal revenue is equal to marginal cost. The price determined at this point is known as equilibrium price and the output produced at this point is called equilibrium output.

How is price determined?

The price of a product is determined by the law of supply and demand. Consumers have a desire to acquire a product, and producers manufacture a supply to meet this demand. The equilibrium market price of a good is the price at which quantity supplied equals quantity demanded.

What is short run in perfect competition?

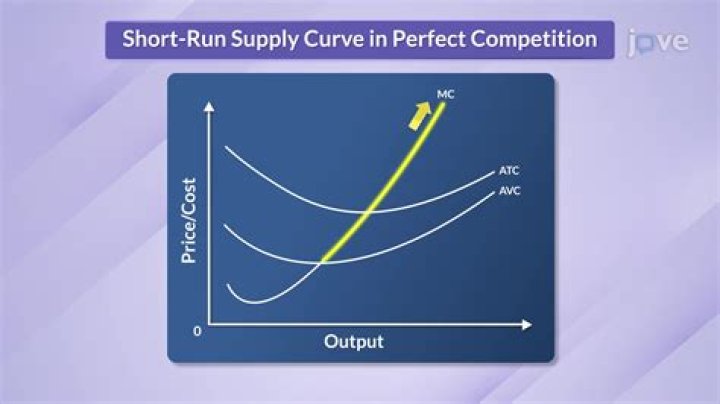

The short-run (SR) supply curve for a perfectly competitive firm is the marginal cost (MC) curve at and above the shutdown point. Portions of the marginal cost curve below the shutdown point are not part of the SR supply curve because the firm is not producing any positive quantity in that range.How the output is determined in short and long run competitive market?

The equilibrium price and output is determined at a point where the short-run marginal cost (SMC) equals marginal revenue (MR). Since costs differ in the short-run, a firm with lower unit costs will be earning only normal profits. In case, it is able to cover just the average variable cost, it incurs losses.

What determines market price and equilibrium output in a market?Equilibrium price and quantity are determined by the intersection of supply and demand. A change in supply, or demand, or both, will necessarily change the equilibrium price, quantity or both. … An increase in demand will create a shortage, which increases the equilibrium price and equilibrium quantity.

Article first time published onHow are prices determined in a planned economy?

Since decision-making is centralized in a command economy, the government controls all of the supply and sets all of the demand. Prices cannot arise naturally like in a market economy, so prices in the economy must be set by government officials.

Who determines the price and quantity traded in a market quizlet?

Prices and quantities traded are determined by the interaction of buyers and sellers in a market. If the price of oranges is too high, the buyer will not purchase them. If the price of oranges is too low, it will not be worth it for the seller to sell them. You just studied 34 terms!

What is price and output determination under perfect competition explain monopolistic competition?

Price-output determination under Monopolistic Competition: Equilibrium of a firm. In monopolistic competition, since the product is differentiated between firms, each firm does not have a perfectly elastic demand for its products. In such a market, all firms determine the price of their own products.

How short run loss minimizing prices and outputs are determined by a monopolistic competitive firm?

In the short run, a monopolistically competitive firm maximizes profit or minimizes losses by producing that quantity where marginal revenue = marginal cost. If average total cost is below the market price, then the firm will earn an economic profit.

How does the monopolist determine his price and output in the short and long period?

A monopolist faces a negative sloping demand curve or AR curve. If he wants to sell more he must lower the price of his product. The corresponding MR curve is also downward sloping and lies below the AR curve i.e., AR > MR.

What happens to prices and output in a perfectly competitive market?

2. In perfect competition, when market demand increases, explain how the price of the good and the output and profit of each firm changes in the short run. When market demand increases, the market price of the good rises, and the market quantity increases. … The firm’s profit rises (or its economic loss decreases).

How does a perfectly competitive company determine its profit maximizing quantity of output?

What two rules does a perfectly competitive firm apply to determine its profit-maximizing quantity of output? Output is determined at the point where price equals marginal cost, and the price is set by the marketplace since the firm is a price taker.

What is perfect competition how pricing decisions are made under perfect competition in short and long run?

The average total cost is of determining importance, since in the long run all costs are variable and none fixed. In the short run a firm under perfect competition is in equilibrium at that output at which marginal cost equals price or Marginal Revenue. This is equally valid in the long run.

How is equilibrium price and quantity determined?

The equilibrium price is the price at which the quantity demanded equals the quantity supplied. Graphically, it is the point at which the two curves intersect. Mathematically, it can be found by setting the demand and supply curves equal to one another and solving for price.

How is market equilibrium determined?

The intersection of the supply and demand curves determines the market equilibrium . At the equilibrium price, the quantity demanded equals the quantity supplied. … Together, demand and supply determine the price and the quantity that will be bought and sold in a market.

What is equilibrium price how it is determined?

Equilibrium price is the price at which both quantity demanded and supplied. of a commodity are equal. • Equilibrium price is determined by the market forces of demand and supply. of a commodity.

How does a planned economy differ from a market economy?

Planned Economy vs Market Economy Planned economy, as denoted by the term, is an economic system that is planned and organized, usually by a government agency. … In contrast, market economies are based on demand and supply. The decisions are taken according to the flow of the free market forces.

Who decides in planned economy?

In a planned economy, the government makes most decisions about what will be produced and what the prices will be, and consumers react passively to that plan. Most economies in the real world are mixed; they combine elements of command and market systems.

What is a planned economy in economics?

Definition of planned economy : an economic system in which the elements of an economy (as labor, capital, and natural resources) are subject to government control and regulation designed to achieve the objectives of a comprehensive plan of economic development — compare free economy, free enterprise.

What type of relationship is between price and quantity in the supply curve?

Price and quantity supplied are directly related. As price goes down, the quantity supplied decreases; as the price goes up, quantity supplied increases. Price changes cause changes in quantity supplied represented by movements along the supply curve.

Is there an inverse relationship between price and quantity demanded?

LAW OF DEMAND – there is an inverse relationship between the price of a good and the quantity demanded by consumers. … In that the price of the good and the quantity demanded are inversely related, the DEMAND CURVE must slope downward to the right.

What does it mean to say that price and quantity demanded are inversely related?

The law of supply and demand is a keystone of modern economics. According to this theory, the price of a good is inversely related to the quantity offered. This makes sense for many goods, since the more costly it becomes, less people will be able to afford it and demand will subsequently drop.

Who determines the price under a monopoly and how is the price determined?

When a monopolist produces the quantity determined by the intersection of MR and MC, it can charge the price determined by the market demand curve at the quantity. Therefore, monopolists produce less but charge more than a firm in a competitive market.

How does a monopolist determine its profit maximizing level of output and price?

A monopolist can determine its profit-maximizing price and quantity by analyzing the marginal revenue and marginal costs of producing an extra unit. If the marginal revenue exceeds the marginal cost, then the firm can increase profit by producing one more unit of output.

How is price determined in a monopolistic market?

The quantity is produced when marginal revenue equals marginal cost, or where the green and blue lines intersect. The price is determined based on where the quantity falls on the demand curve, or the red line. In the short run, the monopolistic competition market acts like a monopoly.

What output and price levels will maximize the firm's profit in the short run?

For a given price (such as P*), the level of output that maximizes profit is the output where marginal cost equals price (Q*), as long as price is greater than average variable cost at that point (in the short run), or greater than average total cost (in the long run). 3.