You can finance 100% of the home price with a USDA loan. However, if you do decide to make a down payment, you can lower your monthly mortgage payments and potentially afford a more expensive home. Are USDA mortgage rates good? USDA loan rates are often lower than conventional 30–year fixed mortgage rates.

How much can you borrow with a Rural Development Loan?

You can finance 100% of the home price with a USDA loan. However, if you do decide to make a down payment, you can lower your monthly mortgage payments and potentially afford a more expensive home. Are USDA mortgage rates good? USDA loan rates are often lower than conventional 30–year fixed mortgage rates.

What are the benefits of a rural development loan?

- A Down Payment Isn’t Required.

- Borrower Qualifications Are More Lenient.

- Less Money Spent On Mortgage Insurance.

- Lower Interest Rates.

- *Remember that only certain property types are USDA-eligible.

Is it hard to get a Rural Development Loan?

Qualification is easier than for many other loan types, since the loan doesn’t require a down payment or a high credit score. Homebuyers should make sure they are looking at homes within USDA-eligible geographic areas, because the property location is the most important factor for this loan type.What is the minimum credit score for a Rural Development Loan?

USDA Loan Credit Score Requirements. The USDA does not set a minimum credit score requirement, but most lenders require a score of at least 640, which is the minimum score needed to qualify for automatic approval using the USDA’s Guaranteed Underwriting System (GUS).

What qualifies for rural development loan?

Minimum Qualifications for USDA Loans At a minimum, USDA guidelines require: U.S. citizenship or legal permanent resident (i.e. U.S. non-citizen national or qualified alien) Ability to prove creditworthiness, typically with a credit score of at least 640. Stable and dependable income.

What FICO score does USDA use?

How the Minimum USDA Credit Score Compares to Other Loans. To qualify for the USDA home mortgage program, you will need a 620 FICO score; some lenders require much higher scores. But, how does the minimum credit requirements compare to other popular types of mortgage loans?

Why would a USDA loan get denied?

Things like unverifiable income, undisclosed debt, or even just having too much household income for your area can cause a loan to be denied. Talk with a USDA loan specialist to get a clear sense of your income and debt situation and what might be possible.Who pays closing costs on USDA loan?

USDA Closing Costs Paid By Seller Rather than bringing more cash to close, USDA loans allow the seller to pay up to 6% of the sales price towards the buyer’s closing costs. Therefore, the seller may pay part or all of the buyer’s closing costs.

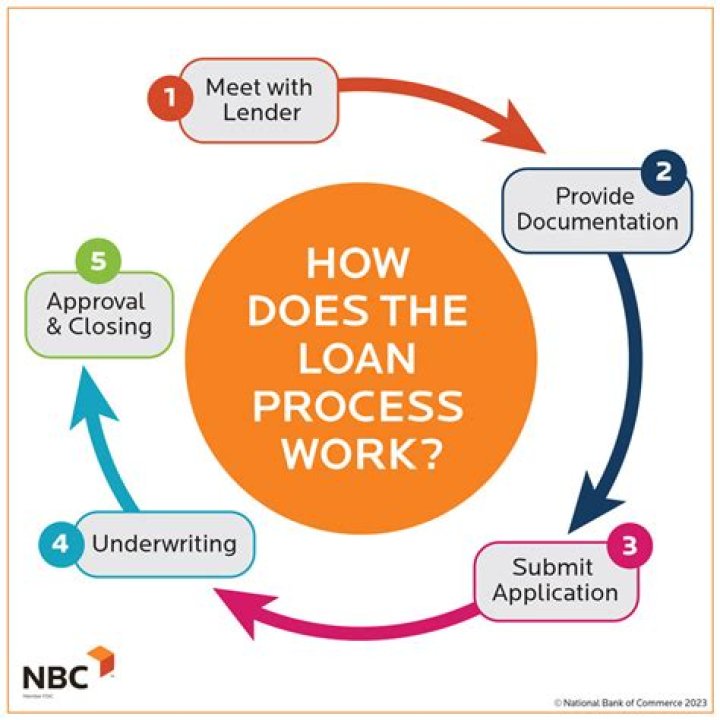

How long does it take to get approved for a Rural Development Loan?Borrowers can typically expect the USDA loan process to take anywhere from 30 to 60 days, depending on the qualifying conditions. Check your USDA loan eligibility here.

Article first time published onDoes USDA pull your credit?

Even if you don’t have a 640 credit score, it’s still possible to apply and be approved for a USDA loan. USDA allows lenders to underwrite and approve USDA home loans manually at the lender’s discretion. Once cleared by your lender, the USDA must review your loan for final loan approval before you can close.

Does USDA require collections to be paid?

USDA does not require medical collection accounts to be paid.

Is USDA funded for 2021?

2021 FUNDING OVERVIEW Funding for mandatory programs is estimated to be $128 billion, $3 billion more than 2020 enacted levels. Including negative receipts, offsetting collections, recoveries, etc., USDA is requesting a total of $146 billion in 2021 available funds.

What are my chances of getting a USDA loan?

To get a USDA loan, you have to meet certain requirements: Your income must be within 115% of the median household income limits specified for your area (find out if you’re eligible here) You must be a U.S. citizen or permanent resident (green card holder) You will likely need a credit score 640 or above.

Can I get a USDA loan with a 550 credit score?

At Nationwide Mortgage & Realty, LLC, the USDA minimum credit score is 550, but other factors are determined during the pre-approval process. Credit scores of 580 or under are not typically approved without strong documentation of extenuating circumstances.

Can I roll closing costs into USDA loan?

Typically, you can’t pay for your closing costs using your loan (also referred to as rolling in your closing costs). However, USDA loans allow borrowers to roll some or all of their closing costs into their mortgages if the home appraises for more than the sales price.

Is homeowners insurance included in USDA loan?

Paying Homeowners and Flood Insurance Premiums For a USDA loan, you have to have homeowners insurance coverage for the amount of the loan or what it would cost to completely replace your house if it was destroyed. … At closing, you will pay the entire first year’s premiums as part of your closing costs.

Can closing costs be rolled into the loan?

Most lenders will allow you to roll closing costs into your mortgage when refinancing. Generally, it isn’t a question of which lender that may allow you to roll closing costs into the mortgage. It’s more so about the type of loan you’re getting – purchase or refinance.

Can a seller deny a USDA loan?

USDA Loans and Seller Concessions Contribution Limits Seller concessions for USDA loans are among the most buyer-friendly out there. Conventional buyers can’t tap into that 9 percent cap unless they’re putting down 20 percent.

How long does USDA commitment take?

Once the USDA office has the file, they generally take up to a week to issue the final commitment and send it back to the bank or lender for closing. This time can greatly change based on the state, volume, etc. But most USDA offices take about 2-7 days.

What is a Certificate of Eligibility from USDA?

The Certificate of Eligibility (COE) informs the applicant about: • Their maximum loan amount based on specified criteria (i.e. county where they wish to live, down payment, taxes, insurance, term, interest rate, and other funding sources).

What is minimum FICO for USDA?

The USDA doesn’t have a fixed credit score requirement, but most lenders offering USDA-guaranteed mortgages require a score of at least 640, and 640 is the minimum credit score you’ll need to qualify for automatic approval through the USDA’s automated loan underwriting system.

Does USDA check medical bills?

With that being said, USDA guidelines have been improved for situations involving medical collections. Current USDA guidelines now instruct the lender to consider the following during the underwriting process: … Medical collections and charge-off accounts must be clearly identifiable on the credit report.

How long does USDA manual underwriting take?

Typically though, borrowers can expect their USDA loans to close in 60 days or less. A loan that is automatically approved for underwriting via GUS may be processed faster.

How many Tradelines are required for USDA?

Applicants with no rent history: Three tradelines are required. Tradelines may be a combination of traditional tradelines from the credit report with 12-month history or eligible non-traditional tradelines.

Who gives money to the USDA?

In addition to federal funding, state and local agencies also administer grants. Monies used to support these programs are obtained primarily through state and local tax revenues and funds received from the federal government (e.g., block and formula grants).

Does USDA run out of funds?

USDA’s fiscal year runs from October 1st until September 30th and at the beginning of each fiscal year, the USDA Single Family Housing Guaranteed Loan Program has a temporary lapse in funding. As a result, we are often asked if a home buyer’s USDA approval time will be affected.

Is USDA out of money?

The USDA fiscal year runs from October 1 through September 30th each year. Typically, USDA is out of funds for about 2 weeks starting October 1. In order for the USDA Rural Development program to exist, it needs government funding. Regretfully, USDA is an annual victim of last-second government negotiations.