You simply need to translate all items of assets and liabilities into the new functional currency using the exchange rate at the date of change. For non-monetary items, this amount will be the item’s new historical cost.

How do you account for change in functional currency?

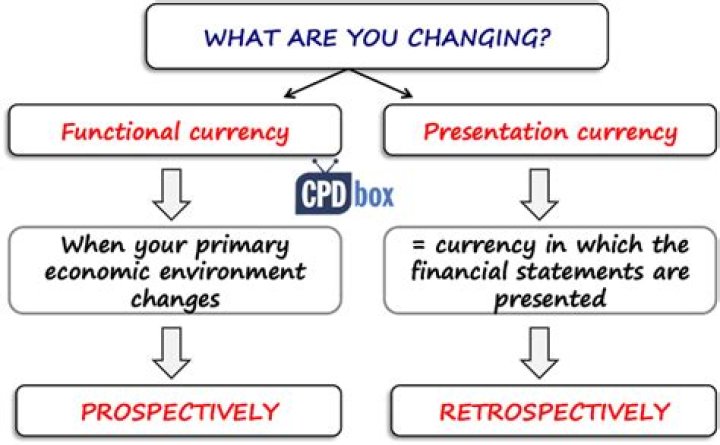

The effect of a change in the functional currency is accounted for prospectively. Therefore, an entity translates all items into the new functional currency using the exchange rate at the date of change. The resulting translated amounts for non-monetary items are treated as their historical cost.

How is a company's functional currency determined?

- Autonomy. Whether the operation is essentially an extension of the reporting entity, or it can operate with a significant degree of autonomy. …

- Proportion of transactions. …

- Proportion of cash flows. …

- Debt service.

When can an entity's functional currency be changed?

As noted in paragraph 15, the functional currency of an entity reflects the underlying transactions, events, and conditions that are relevant to the entity. Accordingly, once the functional currency is determined, it can be changed only if there is a change to those underlying transactions, events, and conditions.Can a branch have a different functional currency?

A Only in rare circumstances will a branch have a different functional currency from its head office. A branch is set up for a purpose and its activities are carried out on behalf of the head office.

Can you have more than one functional currency?

If those operations are conducted in different economic environments, they might have different functional currencies. Therefore, it is possible for a legal entity to have more than one functional currency, assuming it has several distinct and separable operations, each with different functional currencies.

How do I change functional currency in SAP?

On the SAP FIORI dashboard, navigate to Define Currency Settings for Ledgers and Company Codes under Finance -> General Settings -> Currencies. You can find it in the app Manage Your Solution under Configure Your Solution: Finance ->General Setting ->Currencies ->Define Currency Settings for Ledgers and Company Codes.

What is the difference between local currency and functional currency?

The local currency is the national currency of the country where an entity is located. The functional currency is the currency of the primary economic environment in which an entity operates.How do you account for unrealized foreign exchange gains and losses?

The unrealized gains or losses are recorded in the balance sheet under the owner’s equity. It is calculated by deducting all liabilities from the total value of an asset (Equity = Assets – Liabilities).

What is the difference of foreign currency and functional currency?An entity’s functional currency is the currency of the primary economic environment in which the entity operates (ie the environment in which it primarily generates and expends cash). Any other currency is a foreign currency.

Article first time published onWhat do you mean by functional currency?

A functional currency is the main currency that a company conducts its business. As companies transact in many currencies but report their financial statements in one currency, the foreign currencies have to be translated into the functional currency.

What is functional currency example?

Consider the case of the Spanish branch of a U.S. entity. In another circumstance, a Mexican company with most of its operations in the United States would use the U.S. dollar as its functional currency, even if its financial statements are expressed in terms of Mexican pesos. …

How is functional currency IAs 21 calculated?

IAs 21 says that the functional currency is the currency of the primary economic environment in which the entity operates. In most cases, it is crystal clear. Normally, it’s the currency in which the company makes and spends money. And, in most cases it will be just the currency of the country where you operate.

How do you consolidate foreign subsidiaries?

- Make the individual statements of cash flows, separately for a parent and separately for a subsidiary.

- Translate subsidiary’s statement of cash flows to the presentation currency. …

- Aggregate subsidiary’s and parent’s cash flows.

- Eliminate intragroup transactions. …

- Done.

What are the two methods used to translate financial statements and how does the functional currency play a role in determining which method is used?

There are two main methods of currency translation accounting: the current method, for when the subsidiary and parent use the same functional currency; and the temporal method for when they do not. Translation risk arises for a company when the exchange rates fluctuate before financial statements have been reconciled.

How does currency translation adjustment work?

The foreign currency translation adjustment or the cumulative translation adjustment (CTA) compiles all the fluctuations caused by varying exchange rate. Businesses with international operations must translate their transactions like the acquisition of assets or the purchase of services into their functional currency.

How do you change currency reporting?

You can change it, but only for a new fiscal year. To do so, go to General ledger > Currencies > System currency converstion > Ledger reporting currency conversion. Make sure, you test it in a separate environment first.

How do you convert financial statements to currency?

- Determine the functional currency of the foreign entity.

- Remeasure the financial statements of the foreign entity into the reporting currency of the parent company.

- Record gains and losses on the translation of currencies.

How do I change functional currency in Xero?

- Click on the organisation name, select Settings, then click Currencies.

- Click Add Currency.

- Select a currency.

- Click Add Currency.

How do you account for foreign currency transactions?

- all the foreign currency monetary items must be reported at the closing rate. …

- non-monetary items that are carried in terms of historical cost denominated in a foreign currency should be reported using the exchange rate at the date of the transaction; and.

What is the difference between realized and unrealized FX?

But what is the difference between realised and unrealised, and how do they arise? In simple terms, a foreign exchange gain or loss is realised when a transaction is finalised, and unrealised whilst it is still in progress.

How does foreign currency affect financial statements?

Any and all adjustments between a foreign functional currency and the US $ are translation adjustments. Therefore the financial statements will be translated, not remeasured. This means that the affects of changing foreign currency exchange rates will be reflected on the balance sheet and not on the income statement.

What is it called when you transfer currency?

Wire transfers, which are also known as wire payments, allow money to be moved quickly and securely without the need to exchange cash. They allow two parties to transfer funds even if they’re in different (geographic) locations safely. A transfer is usually initiated from one bank or financial institution to another.

Is change in functional currency a change in accounting policy?

In fact, the change in functional currency is NOT the change in accounting policy and therefore the retrospective restatement, i.e. measuring share capital in new functional currency before that change (using the rate at its issuance) would NOT faithfully represent share capital at the time of making a change.

What do you mean by functional and reporting currency?

Functional Currency vs Reporting Currency Functional currency is the currency of the primary economic environment in which the entity operates. Reporting currency is the currency in which financial statements are presented.

Do you Retranslate stock at year end?

Non-monetary items are carried at the historic rate and non-monetary items measured at fair value are translated at the rate of the date when the fair value is re-measured. … Therefore balances covered by a forward contract will be retranslated at the year-end rate.

How do you treat pre acquisition profit?

Revaluation Profit or loss is always treated as capital Profit or Capital Loss i.e. Pre-acquisition Profit or Pre- acquisition Loss, hence, treated accordingly. It will increase the number of shares with the holding company and subsidiary Company.

Can a parent and subsidiary have different year ends?

The maximum allowable difference between the end of your parent company’s reporting period and that of a subsidiary is three months, but it is still advisable to change and match a subsidiary’s reporting date with that of the parent company to enhance accuracy.

How do I create a consolidated profit and loss account?

(i) Consolidated Profit and Loss Account is prepared in a columnar form. On each side there is one column for each company, one column for adjustments and one for total. (ii) Revenue incomes and revenue expenditures of holding company and subsidiary companies are recorded.